In previous blog posts, I have discussed default rules that impact your estate. For instance, if you do not have a Will, then the State statute governing the distribution of your estate will go into operation. In New York, that statute is EPTL § 4-1.1. Your wishes expressed in a valid Will overcome the default rules expressed in the statute, however. Today we are going to discuss assets that are not impacted by either a valid Will or a State statutory schema, and how your selection of a beneficiary distribution scheme will impact who can receive these assets.

If you have an IRA, 401(k), 403(b), an employer-sponsored retirement plan, a life insurance policy, or an annuity contract, then each of these allows for a beneficiary designation. These types of accounts are called "payable on death" (POD) or "transfer on death" (TOD) accounts because they pass directly to your named beneficiaries outside of probate on the event of your death. You may change your beneficiary designations on a POD account at any time, and it is a good habit to review your beneficiary designations on these accounts at least once a year to account for any changes in your life or your family's life.

POD accounts are not controlled by the beneficiary stipulations in your Will, or by the distribution scheme you have selected in your Will, or even by the default provisions in a State statute. They are contracts that you sign with a provider. As such, you are bound by the provisions of the contract and the distribution system found in that contract. We discussed in a prior post the differences between the per capita at each generation distribution system, which is New York's default system if you die without a Will, or a per stirpes distribution system, which you can elect in a valid Will. Each contract that you have signed has a provision that details which distribution system governs that contract. The trick is to understand the distribution provision in your contract(s), and to adjust your estate planning to account for this variable.

Why does this matter? Let's look at an example. Let's imagine that you are a single parent with three children. Your eldest child is also the parent of two children. You have an IRA contract, a POD with beneficiary designations.

Let say that the POD contract's default beneficiary distribution schema is a per capita distribution. Now let's assume that your eldest child predeceases you. What result with a per capita distribution?

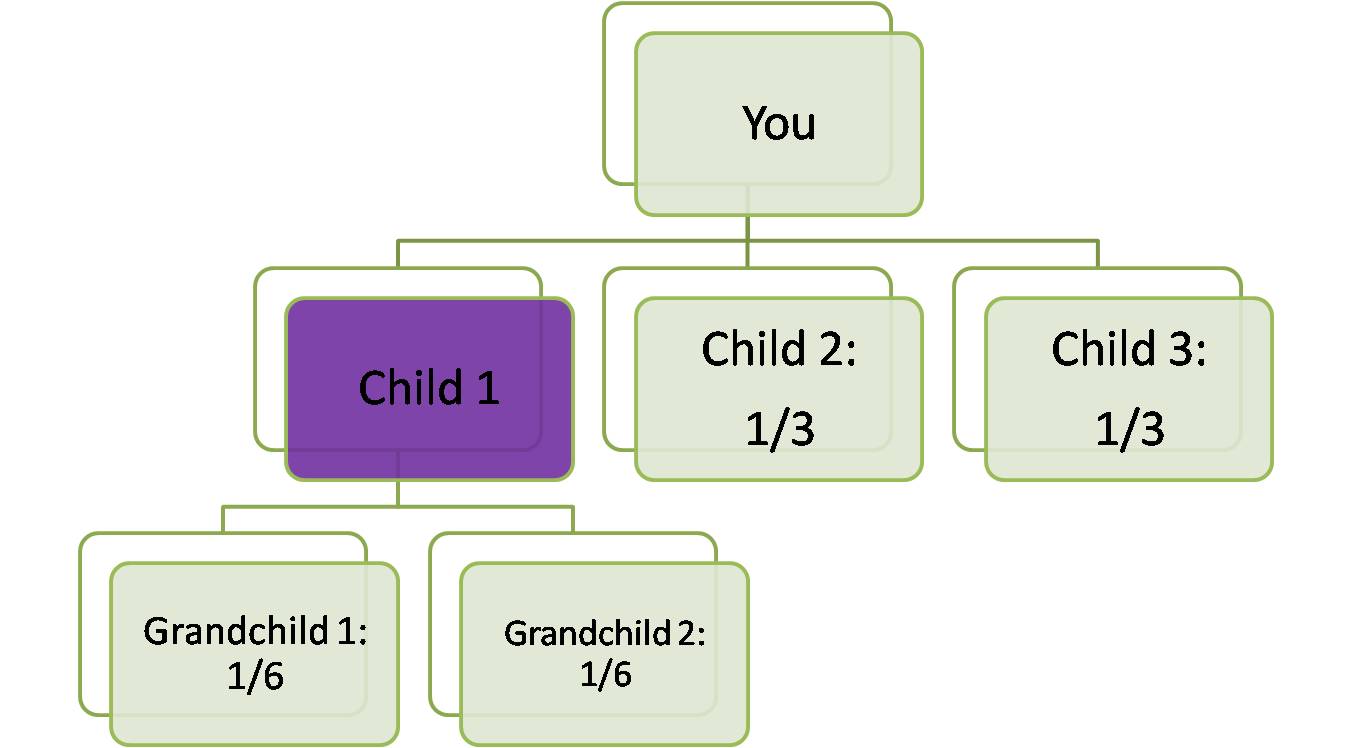

With a per capita distribution, so long as you have living children, none of your assets will be distributed to your grandchildren. If Child 2 also predeceases you, Child 3 will receive 100% of the assets.

Now suppose that your POD contract allows you to select a per stirpes distribution. What result?

With a per stirpes distribution, the 1/3 share that Child 1 would have received is distributed to that child's lineal descendants. Your grandchildren may now receive a portion of your assets.

Reading and understanding the fine print in all of your POD contracts is the first step towards providing for your family's long-term needs. The next step is to reconcile any variations between and among your various POD contracts. To offset these variations in beneficiary distribution schemes, you way wish to consult your attorney to discuss the advantages or disadvantages of naming your estate as the beneficiary on your POD accounts, assuming that you have a valid Will, or a trust that would receive the proceeds of your POD accounts and then distribute these proceeds according to the language of the trust.

In any case, this topic illustrates the need to meet with your attorney on a yearly basis to review your estate plan, including changes in your family, your Will, your POD accounts, and any trust instruments that you may have drafted. These are complex matters that require professional knowledge and attention to detail. This is a yearly appointment that you don't want to miss because it will ensure the continued welfare and well-being of your loved ones.

I invite you to join my list of subscribers to this blog by clicking on "Subscribe to" on the left-hand side of the page so that you can receive a notification when the next installment has been published. Thank you.

I invite you to join my list of subscribers to this blog by clicking on "Subscribe to" on the left-hand side of the page so that you can receive a notification when the next installment has been published. Thank you.

No comments:

Post a Comment